Insurance for High-Risk Occupations

In the realm of insurance, high-risk occupations present a unique challenge. These jobs involve inherent dangers that significantly increase the likelihood of accidents, injuries, or even fatalities. Consequently, securing insurance for individuals in these professions can be more complex and costly. This article delves into the intricacies of insurance for high-risk occupations, examining the types of coverage available, the challenges faced by both insurers and insured, and strategies to mitigate risks.

Understanding High-Risk Occupations

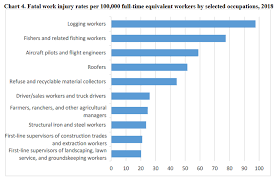

High-risk occupations are those where workers are exposed to significant hazards. Examples include construction workers, miners, firefighters, law enforcement officers, pilots, and commercial fishermen. These professions often involve dangerous equipment, hazardous environments, or physically demanding tasks that elevate the risk of injury or death.

Types of Insurance for High-Risk Occupations

- Life Insurance: Life insurance for individuals in high-risk occupations often comes with higher premiums due to the increased likelihood of a claim. However, it is crucial for providing financial security to the family members of the insured in the event of a fatal accident.

- Disability Insurance: Disability insurance is essential for high-risk workers as it provides income replacement if they are unable to work due to an injury or illness. This type of insurance can be short-term or long-term, depending on the nature and severity of the disability.

- Health Insurance: Comprehensive health insurance is vital for high-risk workers to cover medical expenses resulting from work-related injuries. Given the higher probability of accidents, having robust health insurance can alleviate financial burdens associated with medical treatments and rehabilitation.

- Workers’ Compensation Insurance: Employers are typically required to provide workers’ compensation insurance, which covers medical expenses and lost wages for employees injured on the job. This insurance is particularly important in high-risk occupations where workplace injuries are more common.

- Occupational Hazard Insurance: This specialized insurance covers specific risks associated with certain high-risk occupations. For example, professional divers may need coverage for decompression sickness, while pilots might require insurance for aviation-related accidents.

Challenges in Insuring High-Risk Occupations

- Higher Premiums: Insurers charge higher premiums for high-risk occupations due to the increased likelihood of claims. This can make it challenging for workers to afford adequate coverage.

- Limited Coverage Options: Some insurers may refuse to provide coverage for certain high-risk occupations, limiting the options available to these workers. This lack of competition can further drive up the cost of insurance.

- Stringent Underwriting: Insurers often employ stringent underwriting processes to assess the risk associated with high-risk occupations. This can lead to delays in obtaining coverage and may result in exclusions or limitations in the policy.

- Exclusions and Limitations: Insurance policies for high-risk occupations often come with exclusions and limitations. For instance, a policy might exclude coverage for injuries sustained while operating heavy machinery or limit the payout for certain types of accidents.

Mitigating Risks and Reducing Insurance Costs

- Safety Training and Education: Employers can invest in safety training and education programs to reduce the likelihood of accidents. Well-trained workers are less likely to make mistakes that could lead to injuries, thereby lowering the risk profile of the occupation.

- Implementing Safety Protocols: Adopting and strictly enforcing safety protocols can significantly reduce workplace hazards. This includes providing personal protective equipment (PPE), conducting regular safety drills, and maintaining machinery and equipment properly.

- Wellness Programs: Employers can implement wellness programs to promote the overall health and well-being of their employees. Healthy workers are less likely to suffer from illnesses that could exacerbate the risks associated with high-risk occupations.

- Leveraging Technology: The use of technology, such as wearable safety devices and advanced monitoring systems, can help in early detection of potential hazards and prompt preventive measures. This can reduce the incidence of accidents and injuries.

- Seeking Professional Advice: Consulting with insurance brokers or financial advisors who specialize in high-risk occupations can help workers identify the best insurance options. These professionals can navigate the complexities of the insurance market and find policies that offer comprehensive coverage at competitive rates.

Conclusion

Insurance for high-risk occupations is a critical component of financial planning for individuals engaged in dangerous professions. While the increased premiums and limited coverage options present challenges, understanding the types of insurance available and implementing risk mitigation strategies can help high-risk workers secure the protection they need. Employers and employees alike must prioritize safety and seek professional advice to ensure that adequate coverage is in place, safeguarding their financial future in the face of occupational hazards.